What to Watch for in Archer-Daniels-Midland’s Upcoming Earnings Report

info Adjust the font size of this article to get the best reading experience.

Archer-Daniels-Midland Company (ADM) is a leading global food processing and commodities trading company with a market capitalization of $38.8 billion. Based in Chicago, Illinois, ADM provides a wide range of agricultural, nutrition, and ingredient solutions for both human and animal consumption across multiple international markets. The company operates through three primary segments: Ag Services and Oilseeds; Carbohydrate Solutions; and Nutrition. These segments offer products such as oilseeds, vegetable oils, plant-based proteins, probiotics, and specialty food ingredients.

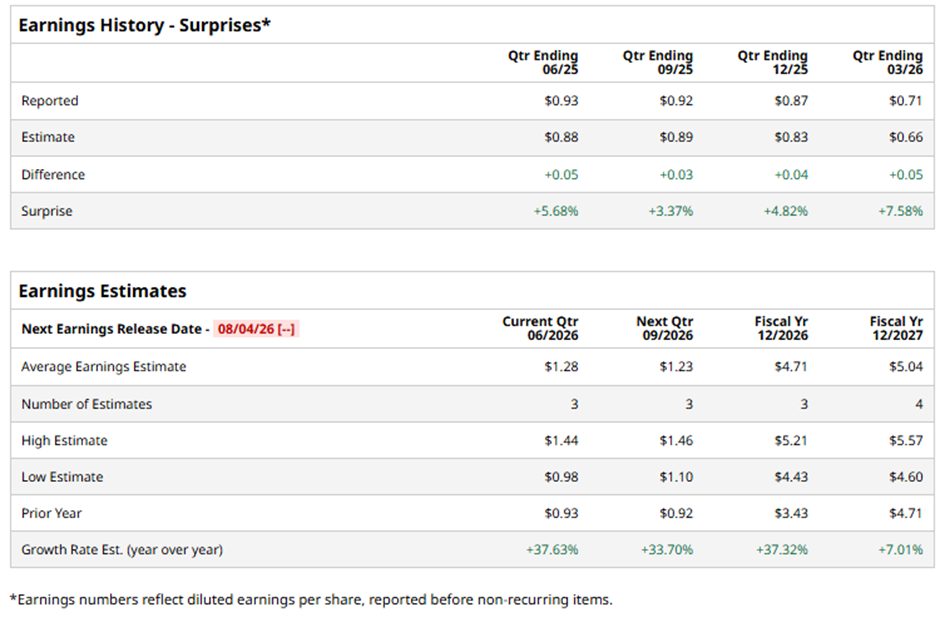

The company is preparing to announce its fiscal Q2 2026 results, which are expected to show strong performance. Analysts anticipate that ADM will report an adjusted EPS of $1.28 for the quarter, a significant increase from $0.93 in the same period last year. This represents a 37.6% growth. In the past four quarters, ADM has consistently exceeded Wall Street’s earnings estimates, indicating strong financial performance.

Looking ahead, analysts forecast that ADM will post an adjusted EPS of $4.71 for fiscal 2026, a substantial increase from $3.43 in fiscal 2025. This represents a 37.3% growth, reflecting the company’s continued expansion and profitability.

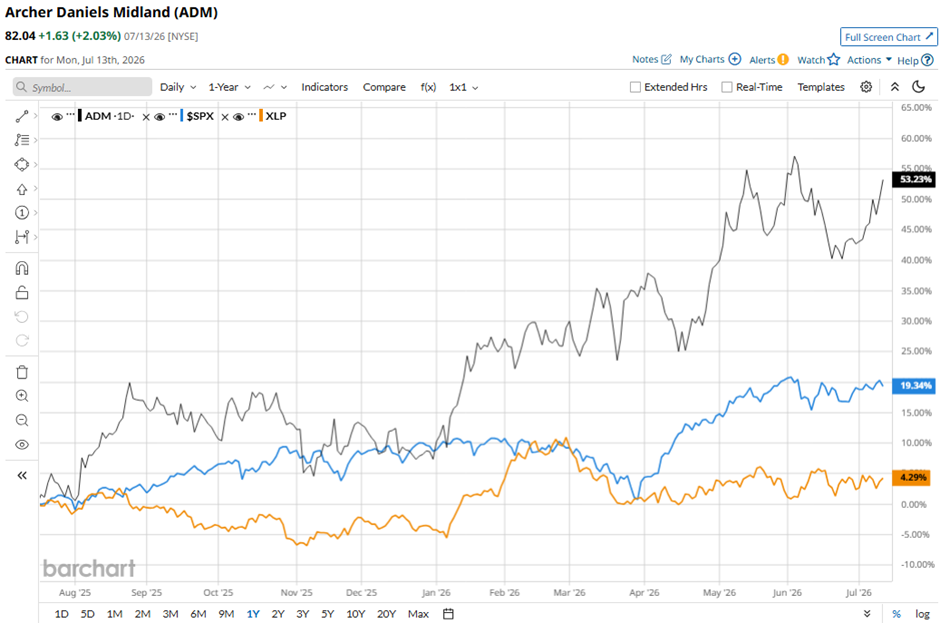

Over the past 52 weeks, ADM stock has surged by 49.3%, outperforming both the S&P 500 Index, which gained 20.1%, and the State Street Consumer Staples Select Sector SPDR ETF, which rose by 4.7%. This impressive performance highlights investor confidence in the company’s long-term prospects.

On May 5, shares of Archer-Daniels-Midland increased by 3.8% after the company reported stronger-than-expected Q1 2026 results. The quarter saw an adjusted EPS of $0.71, net earnings of $298 million, and a 2% rise in total segment operating profit to $764 million. The company also raised its full-year 2026 adjusted EPS guidance to between $4.15 and $4.70. This increase was primarily driven by expected improvements in its crushing and ethanol businesses, supported by favorable U.S. biofuels policy changes.

The positive performance was further bolstered by strong segment results. The Carbohydrate Solutions segment saw a 48% jump in operating profit to $356 million, while the Nutrition segment experienced a 42% increase in operating profit to $135 million. These gains helped offset a 34% decline in Ag Services & Oilseeds profit, which was impacted by approximately $275 million in negative mark-to-market and timing effects.

Despite the strong performance, analysts remain cautious about ADM stock, with an overall “Hold” rating. Among the 10 analysts covering the stock, one recommends “Strong Buy,” six suggest “Hold,” one advises “Moderate Sell,” and two recommend “Strong Sell.” As of the latest data, ADM is trading above the average analyst price target of $78.11.

For more information, readers can refer to the Daily News Lite Disclosure Policy. The article includes only informational purposes and does not constitute financial advice. Additional news from Daily News Lite includes comparisons between retail giants like Costco and Walmart, insights on SK Hynix stock from Jim Cramer, and updates on CF Industries’ dividend increase and stock performance. Readers can also stay informed with the FREE Daily News LiteBrief newsletter, which offers midday updates on stock movements, sector trends, and investor sentiment.

- Author: Tyo Murty

At the moment there is no comment